I Thought We Were Covered: The 4 Trucking Insurance Policies Every Owner-Operator Must Understand

By Ray Kowalski / HaulSmarterHQ Editorial / Published June 17, 2026 · Insurance · 9 min read

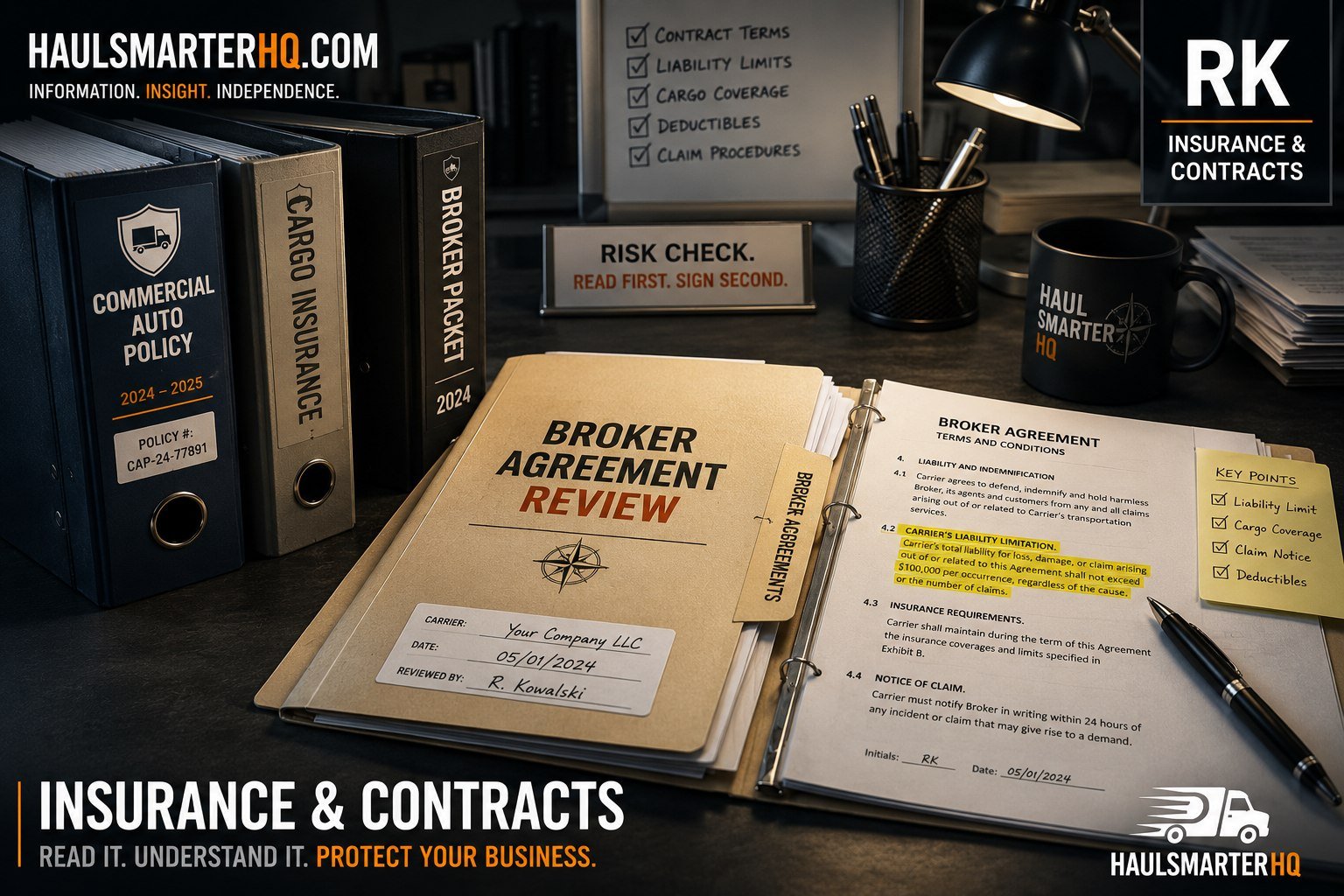

The most expensive words in this business are: “I thought we were covered.”

I have watched operators sign a policy, file it in the glovebox, and never read a single page of it until the day they needed it. That is the worst possible day to find out what your insurance actually does. By then the loss already happened, the adjuster already has your file, and the gap in your coverage is now a number with your name on it.

So let’s do the boring thing that saves operators thousands of dollars: let’s actually read the policy. Not the whole thing tonight — just enough that you understand the four coverages you are paying for, where the holes usually are, and the exact questions to put to your broker before you renew.

The Four Trucking Insurance Coverages You Are Actually Buying

When people say “trucking insurance,” they are usually talking about one bill that bundles several very different protections. Each one covers a different kind of bad day. Mixing them up is where operators get hurt, because they assume one of them covers a loss that actually belongs to another — and that other one is the coverage they skipped to save money.

Here is the plain-English version of what each piece does.

| Coverage | What it actually pays for | Who it protects |

|---|---|---|

| Primary Liability | Damage and injuries you cause to other people and their property in an accident | The other guy (and your legal exposure to him) |

| Cargo Insurance | The freight you are hauling, if it is damaged, lost, or stolen in your care | The shipper’s goods on your trailer |

| Physical Damage | Your own truck and trailer, from collision or other covered events | Your equipment |

| Non-Trucking / Bobtail | Liability when you are driving without a load and not under dispatch | You, on personal or off-dispatch miles |

Read that table twice. The single most common misunderstanding in this whole business lives inside it: primary liability does not pay to fix your own truck, and it does not pay for the freight. It pays for the damage you do to other people. That is it. If you put your truck in a ditch by yourself with a load of electronics on board, liability does nothing for you. Physical damage covers the truck. Cargo covers the electronics. Liability sits there quietly because nobody else was involved.

Most operators can name these coverages. Far fewer can tell you which one actually pays when something goes wrong. That distinction matters more than most people realize. The truck does not care what you thought was covered. The adjuster does not care either. When a claim happens, every dollar gets sorted into a specific bucket, and if the loss does not belong in the bucket you thought it did, the difference becomes your problem. Let’s make sure that doesn’t happen.

Liability: The One the Law Makes You Carry

Primary liability is the coverage FMCSA requires before you can run under your own authority — generally a minimum of $750,000, though most shippers and brokers will not touch you under $1,000,000. It pays when you are at fault for bodily injury or property damage to others.

Here is what operators miss: the legal minimum is a floor, not a recommendation. A single serious injury accident can generate medical and legal claims well past a million dollars. If the judgment exceeds your limit, the difference does not disappear — it comes out of you. Your truck, your house, your future earnings. The premium you save buying the minimum is real money today; the gap you are carrying is a much bigger number you cannot see yet.

Cargo: Smaller Than You Think, and Full of Exclusions

Cargo insurance is where I see the most painful surprises, because operators assume “I have cargo coverage” means “anything on my trailer is covered.” It does not. Cargo policies are built out of exclusions, and the exclusions are where the money is.

Common things a standard cargo policy may not cover, or covers only with a specific endorsement:

| Often Excluded or Limited | Why it matters |

|---|---|

| Reefer breakdown | If your reefer unit fails and the load spoils, many policies will not pay without a reefer breakdown endorsement |

| Unattended vehicle theft | Leave the truck running at a truck stop and a theft claim can be denied |

| Specific commodities | Electronics, pharmaceuticals, alcohol, tobacco and other high-theft items are often restricted |

| Contamination | One load contaminating another can fall outside standard coverage |

The dollar limit matters as much as the exclusions. Let me show you exactly how this plays out, because the number is what people remember.

The Load That Ends an Operator

| Item | Amount |

|---|---|

| Electronics load accepted | $180,000 |

| Cargo policy limit | $100,000 |

| Insurance payout after total loss | $100,000 |

| Remaining exposure | $80,000 |

| Cargo deductible | $2,500 |

| Possible legal costs | Open-ended |

Eighty thousand dollars, out of your pocket, on a load you were proud to land that morning. You do not get to find that out at delivery. You find it out the day it burns.

Physical Damage: Protecting Your Own Iron

Physical damage is the coverage for your truck and trailer. It is optional in the eyes of the law, but if you still owe money on the truck, your lender will require it.

The two things to understand here are how they value your truck and your deductible.

“Actual cash value” means they pay what the truck is worth today, depreciation included — not what you owe and not what it costs to replace.

If you owe more than the truck is worth, that gap is yours unless you carry gap coverage.

And a deductible you cannot actually afford to pay is not a saving; it is a coverage you cannot use.

The Gaps That Quietly Put Operators Out of Business

Most operators do not get hurt by the coverage they bought. They get hurt by the gap between two coverages.

| The Gap | What Goes Wrong |

|---|---|

| Bobtail gap | Liability may not apply while off-dispatch |

| Trailer interchange gap | Borrowed trailer may not be covered |

| Cargo limit gap | Load value exceeds cargo limit |

| Deductible gap | Deductible too large to realistically use |

| Lapse gap | Missed payment cancels coverage |

Questions to Put to Your Broker Before You Renew

You do not need a law degree to protect yourself. You need answers. Take this list to your broker:

| Ask Your Broker | Why You’re Asking |

|---|---|

| What is my exact liability limit? | Identify exposure above limits |

| What is my cargo limit? | Verify load values are covered |

| What commodities are excluded? | Avoid denied cargo claims |

| Am I covered off-dispatch? | Verify non-trucking coverage |

| Do I have reefer breakdown coverage? | Prevent reefer claim surprises |

| What are my deductibles? | Confirm affordability |

| Is a borrowed trailer covered? | Check trailer interchange exposure |

Ray’s 5-Minute Coverage Check

Ask yourself right now:

- Do I know my liability limit?

- Do I know my cargo limit?

- Do I know my deductible on each coverage?

- Am I covered off-dispatch?

- Do I know what commodities my cargo policy excludes?

If any answer is “No,” call your broker this week. Not next renewal. This week.

The Bottom Line

Insurance is not a bill you pay to make the truck legal. It is the thing standing between one bad day and the end of your business.

The operators who survive a serious loss are almost never the ones who got lucky. They are the ones who read the policy before they needed it, knew exactly where their gaps were, and either closed them or accepted them knowingly.

Pull your policy out this week. Find your limits. Find your deductibles. Ask the questions.

Because the most expensive words in business are still: “I thought we were covered.”

Free Download: Insurance Renewal Checklist for Owner-Operators

Before your next renewal, run through the same checklist I would. Inside:

- Coverage limits worksheet

- Cargo limit worksheet

- Deductible review

- Broker question list

- Renewal review checklist

This article is general educational information about commercial trucking insurance and is not insurance, legal, or financial advice. Coverage terms, limits, exclusions, and requirements vary by policy, carrier, commodity, and state. Always review your actual policy and consult a licensed insurance professional before making coverage decisions.