The Insurance Renewal Checklist: What to Review Before You Sign for Another Year

By Ray “Show Me the Contract” Kowalski / HaulSmarterHQ Editorial / Published June 19, 2026 · Insurance · 10 min read

Renewal season is when most owner-operators make the most expensive decision of their year without realizing they are making it.

Here is how it usually goes. The renewal notice arrives. The premium went up. You call around, somebody quotes you a number a little lower, you move the policy to save forty dollars a month, and you sign. Done for another year. You never opened the policy. You never compared what the cheaper one actually covers. You bought a price, not a coverage.

Then, eight months later, something goes wrong — a cargo claim, a jackknife, a trailer full of freight that did not survive a reefer failure — and you find out the cheaper policy had a hole in it exactly where you needed it not to. The forty dollars you saved becomes the forty thousand you owe.

So before you sign for another year, do the boring thing that saves operators more money than any rate negotiation ever will: actually review what you are renewing. This is the checklist I walk every operator through. None of it requires a law degree. All of it requires that you read before you sign.

Can you answer these right now, without opening your policy?

✓ Your cargo coverage limit

✓ Your physical damage deductible

✓ Your largest cargo exclusion

✓ Whether your bobtail coverage is active

If you cannot answer all four, review your policy before you renew. This article walks you through each one.

Start With What You Actually Have Now

Before you can judge a renewal offer, you need to know what your current policy really does — not what you think it does. Pull the declarations page, the part that lists your coverages and limits, and put a real number next to each line.

You are looking for four things you are paying for: primary liability, which pays for damage and injury you cause to other people; physical damage, which pays to fix or replace your own truck and trailer; cargo coverage, which pays for the freight you are hauling when it is damaged, lost, or stolen; and non-trucking or bobtail liability, which covers you when you are driving without a load and off dispatch. If you cannot say, from memory, roughly what each of those limits is, that is the first sign you have been renewing on price instead of coverage.

The Renewal Checklist at a Glance

Here is the whole review on one page. The sections below walk through each line in plain English.

| Coverage | What to Verify | Why It Matters |

|---|---|---|

| Primary Liability | Limit still correct for your freight | It is federally required and your largest premium line |

| Physical Damage | Stated value and deductible | Prevents overpaying and surprise out-of-pocket costs |

| Cargo | Exclusions reviewed against your freight | Exclusions are the top reason claims get denied |

| Bobtail / Non-Trucking | Coverage active and clearly defined | Protects you when driving off dispatch |

The Coverage Review: Line by Line

Here is what to check on each piece before you agree to carry it for another twelve months.

Primary Liability

This is the coverage the federal government requires before you can run under your own authority, and it is usually your largest premium line. The number to confirm is the limit — most operators carry the standard limit required for their freight, but if your operation changed this year, your required limit may have changed too. The question for your broker: given the freight I am actually hauling now, is my liability limit still correct, or am I carrying a limit that no longer matches my operation?

Physical Damage

This covers your own equipment. The two things that quietly erode this coverage are the deductible and the stated value. If your truck is a year older than it was at the last renewal, its value dropped — make sure you are not paying to insure a value the truck no longer has. And look hard at the deductible, the amount you pay out of pocket before coverage kicks in. A low premium often hides a high deductible, which means a small claim is entirely on you anyway.

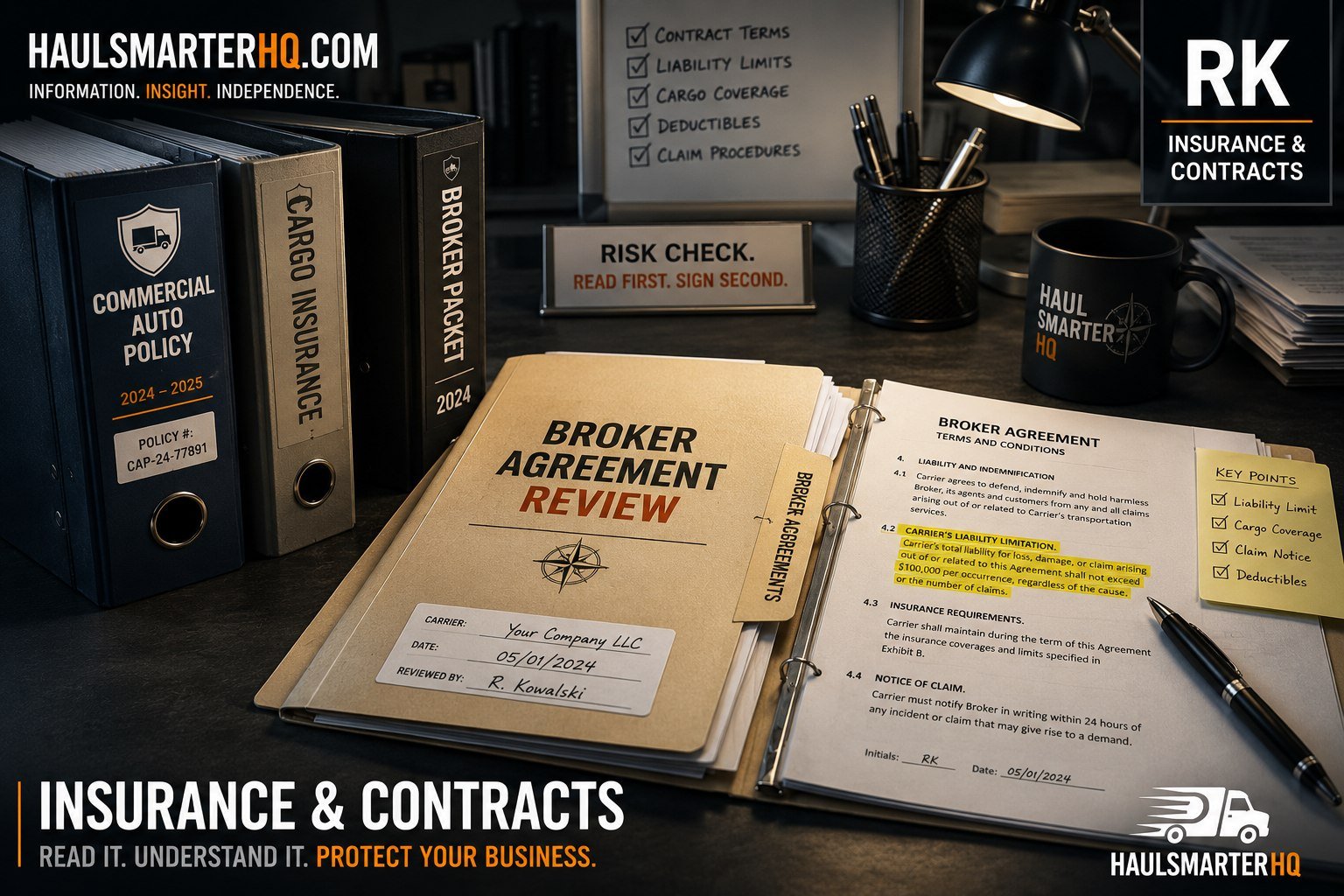

Cargo Coverage

This is where the most painful surprises live, because cargo policies are full of exclusions — specific situations the policy will not pay for. The classic one is the reefer breakdown clause: if you haul refrigerated freight, many policies only cover a spoilage loss if the unit was serviced and inspected on a set schedule, and if you cannot prove you kept that schedule, the claim is denied. Other common exclusions cover certain commodities, unattended vehicles, and theft under specific conditions. The question for your broker: read me the exclusions, out loud, and tell me which ones apply to the freight I actually haul.

Non-Trucking and Bobtail Liability

This is the small, cheap coverage everybody forgets until they need it. It covers you when the truck is moving but you are not under dispatch — driving home, heading to the shop. If you do not have it, a single accident on a personal trip in your truck can become entirely your problem. Confirm it is on the policy and that the line between “under dispatch” and “not under dispatch” is clear.

The Words That Decide Whether a Claim Gets Paid

Beyond the four coverages, a handful of terms in the policy decide how a claim actually plays out. You do not need to master them — you need to know they exist and ask about them.

The deductible is what you pay before the insurer pays anything; a higher one lowers your premium but raises your risk on every claim. An exclusion is anything the policy specifically will not cover, and it is the single most common reason a claim that “should have been covered” is denied. An endorsement is an add-on or change to the standard policy, and a cheaper policy sometimes gets cheaper by quietly removing an endorsement you had before. Subrogation is the insurer’s right to go recover money from whoever was actually at fault after they pay you — relevant because it affects how your claim and your premium are handled afterward. And an additional insured requirement, often buried in your broker or shipper contracts, can obligate you to extend your coverage to another party, which your policy has to actually allow.

The Renewal Conversation to Have Before You Sign

When the renewal offer is in front of you, the goal is simple: do not compare two premiums, compare two coverages. A lower number means nothing until you know what was removed to get there.

Put these questions to your broker, and get the answers in writing, not over the phone where they evaporate. What changed between my expiring policy and this renewal — coverages, limits, deductibles, exclusions, all of it? If this renewal is cheaper, what was reduced or removed to make it cheaper? Given the freight and lanes I actually run now, where is my biggest uncovered gap? And if I had a total loss tomorrow, walk me through exactly what this policy would and would not pay.

An honest broker will answer all four without flinching. If you get vague answers, that is information too.

Read Before You Sign

Insurance is not a product you buy once and forget. It is a contract you re-sign every year, and every renewal is a chance to either close a gap or quietly open one. The operators who lose forty thousand dollars almost never lose it to a freak accident. They lose it to a clause they never read, in a policy they renewed on price, on a day when nothing felt urgent.

So this year, before you sign, do the boring thing. Pull the policy. Check the four coverages. Ask the four questions. Get it in writing. It is an afternoon of work that can stand between a bad week and a bankruptcy.

Show me the contract — before you sign it, not after it ruins you.

Your 30-Minute Renewal Review

If all you have is half an hour before you talk to your broker, spend it on the parts that actually decide claims. Read the four coverages on your declarations page and confirm each limit still fits your operation. Read the cargo exclusions and mark the ones that apply to the freight you actually haul. Then walk in with the four questions: what changed, what was cut to lower the price, where is my biggest gap, and what would this policy pay on a total loss. The deductibles, endorsements, and fine print matter too, but if you are short on time, the four coverages, the four questions, and your specific exclusions are the review. Everything else is secondary.

Do not walk into your renewal without it.

The exact coverage-by-coverage checklist Ray uses — limits, deductibles, exclusions, and the questions to put to your broker before you sign for another year.

Get the Insurance Renewal Checklist →